Nick's Market Notes:

WINTER 2026

It's the end of a cycle that COVID, record low interest rates, combined with high population growth artificially accelerated. The market is no longer driven by momentum, but by fear, realism, and selectivity.

A blend of pessimism and optimism is creating a disjointed market. A house one week may get multiple offers, where a similar home a couple weeks later may get none. Uncertainty remains the dominant theme and it is hard to read the news today and believe 2026 will be any different. (does the world need to wait this out or is this a new normal?). Having said that, COVID reinforced an important lesson: people adapt, normalize risk, and eventually re-engage.

Recent Market Context

The Toronto real estate market entered 2025 on relatively steady ground, with average prices holding compared to the year prior. While there were early concerns around trade, expectations were generally for prices to remain stable or appreciate modestly.

That shifted on April 2nd or “Liberation Day,” when trade uncertainty intensified and sentiment weakened. As the year progressed, uncertainty took over and the market continually softened.

Inventory, Pricing, and Seller Behaviour

There is increasing commentary around whether this will finally be the year that long-time holdouts come to market. Early signs suggest movement, as Toronto 2026 is starting off much quicker than last year, with roughly 2X the number of 'new' freehold listings.

There is plenty of overpriced inventory currently on the market. Many sellers remain unwilling to capitulate, which masks underlying weakness and extends selling timelines.

Condos, Freehold, and Liquidity Dynamics

Condo depreciation appears to be stabilizing, while depreciation in the freehold market accelerated in 2025. In Toronto, the stalled condo market had broader implications on this acceleration of depreciation in freehold homes. Liquidity is trapped, limiting move-up activity and dragging down freehold prices.

Investors and first-time buyers continue to drive the condo market, but the rent versus own math isn't as attractive as it once was. That said, early signs of downtown office recovery in the fourth quarter are a modest positive for the condo market and the broader Toronto market. I view a decline in commercial office vacancy as a valuable leading indicator.

I do not expect the broader freehold market to rebound materially without sales rebounding in the condo market. As such, condo prices stabilizing downtown is a positive.

Geographic Preferences

I continue to favour the Toronto market over the suburbs, purely for the employment opportunity, but that doesn't mean there aren't great opportunities that wouldn't otherwise exist in some sought after locations/neighbourhoods outside of town. The 905 condo market and suburbs remain vulnerable, particularly in trade-sensitive cities and towns where employment and investor demand are more exposed to macro shocks, (ex. autos/steel).

Macro Backdrop and Cross-Asset Signals

In contrast to real estate, stock market strength is broadening beyond technology, forming what feels like a hyper bull market. U.S. GDP growth is expected to be very strong in 2026, though this growth is occurring alongside higher debt levels and a weakening U.S. dollar.

The Canadian dollar may appreciate materially as a result. Canada’s economy has shown resilience in the face of tariffs, supported in large part by CUSMA. Whether through renegotiation or the absence of a new deal, CUSMA in 2026 appears likely to reinforce the status quo of uncertainty. Based on a recent speech(s), it looks like we are gearing up for a tough negotiation.

A favourable or at least livable trade outcome could act as a meaningful mid to long-term catalyst. At my most optimistic, I believe there is a world where Carney maneuvers around Trump and Canada ultimately comes out of this stronger with more diversified global trade. However it happens, a normalization of risk will spur investment, the job market, and help people to feel more confident about the future.

Rates, Credit, and External Risks

A record number of mortgage renewals are scheduled for 2026. Previous fears of mortgage renewals crashing the market have been unfounded due to the strict mortgage qualification process in Canada. A contrarian view: the next interest rate move may be up, not down.

External political factors matter. Trump-related actions or rhetoric could bring more volatility. Volatility often creates opportunity for prepared buyers.

Behavioural Shifts and Lifestyle Choices

People appear to be prioritizing travel, entertainment, and experiences. Spending on oneself has taken precedence over large financial commitments for many households.

Opportunities and Risk-Reward

Opportunities for deal-making continue to exist in underappreciated homes, including properties requiring cosmetic updates, fixers, investor-oriented assets, and multi-unit opportunities.

Contrarian idea: selectively re-entering the cottage and recreational market in 2026, as well as the Toronto core condo market. The risk-reward profile is becoming more compelling for those attempting to time the market.

The resilience of the Canadian economy and the relative strength and mandate of leadership thus far are providing a degree of confidence. For the disciplined, risk-reward is improving.

Execution Matters More Than Ever

Selling with a clear plan is more important than ever. If you own a home, it will sell. Panic and drastic course corrections are rarely rewarded.

Be open to new ideas, select the best plan, and follow the process. And finally, a reminder from experience: a good Realtor is also a good therapist.

Written Jan 23, 2026

Thoughtful Toronto Real Estate Predictions

Nick's Market Notes:

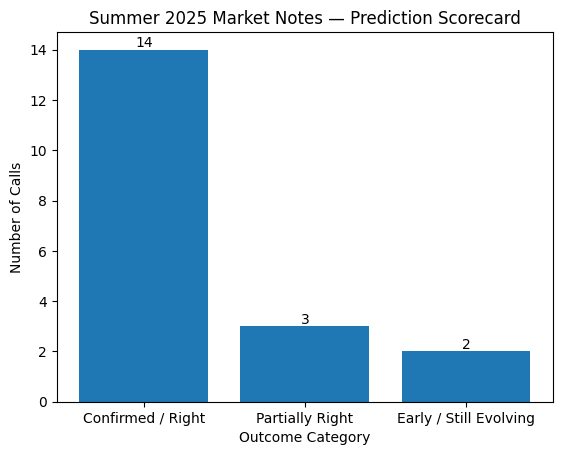

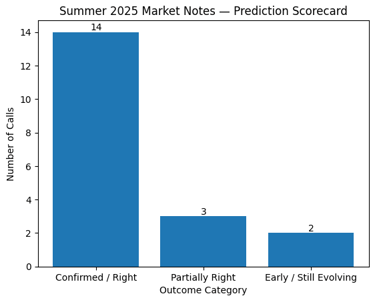

Summer 2025 - Reviewed

Unique homes and boutique condos would hold value.

✅ Right

Distinctive freeholds and livable, low-density condo buildings continued to outperform generic product. Buyers stayed selective, but originality and strong layouts still commanded attention and pricing power.

Turn-key, family homes in strong neighbourhoods would remain the gold standard. ✅ Right

Buyers consistently paid premiums for certainty. Renovation fatigue, higher construction costs, and time risk made move-in-ready homes even more attractive.

The 416 would outperform the 905. ✅ Right

The pricing and liquidity gap widened, particularly as peripheral markets struggled with affordability sensitivity and investor pullback.

Newer, investor-heavy GTA subdivisions would face pressure.

✅ Right

This became one of the weakest segments. End-user demand was thin, resale competition was heavy, and price support proved fragile.

Peripheral markets could see depreciation if rates stayed elevated. ⚠️ Partially right

Not uniform, but softer demand and longer selling times became more common as carrying costs stayed high.

Rising 416 listings would not equal a flood of quality homes.

✅ Right

Inventory increased, but much of it was compromised by pricing, layout, or location. Well-priced, well-located homes still sold. The rest sat.

Condos would continue to underperform. ✅ Right

The condo market remained the softest major asset class, particularly investor-driven high-rise product.

Boutique and functional condo layouts would outperform investor stock. ✅ Right

Larger, livable units consistently outperformed small, uniform investor units where resale competition was fiercest.

Investor capital would remain trapped in condos.

✅ Right

This limited mobility and muted recovery, especially in the pre-construction and resale investor segments.

Equity market strength would provide a modest confidence tailwind. 🕰️ Mildly right, still evolving

Strong equity markets helped certain homeowners absorb higher rates, though this did not materially improve buyer affordability.

Back-to-office mandates would quietly support downtown demand. 🕰️ Early confirmation

This supported sentiment and leasing more than sales, reinforcing the relative strength of the 416 core versus fringe markets.

Toronto would outperform surrounding regions in a downturn.

✅ Right (so far)

Job diversity and liquidity continued to favor the city over commuter and recreational markets.

Downtown office recovery would be uneven. ✅ Right

Leasing improved at the top end, but large-block vacancies persisted, keeping recovery fragmented.

Recreational markets would remain soft. ✅ Right

Demand stayed muted outside prime lakes and established towns.

Prime cottage locations would outperform remote markets.

✅ Right

Drive time and established communities mattered more than ever.

Subdivisions would remain a tough sell. ✅ Right

Buyers consistently favored character and walkability over homogeneity.

Best buying opportunities would be fixers, estate sales, larger condos, and gentrifying areas. 🕰️ Still valid

These remain the most compelling value plays for patient buyers.

Leasing would favor larger, well-laid-out units. ✅ Right

Functional rentals leased faster and with less friction.

Fundamentals would matter more than ever. ✅ Fully confirmed

The market rewarded preparation and punished shortcuts. There was no bailout for poor product or pricing.

Originally sent January 18, 2025. Verdicts based on August 2025 data and trends.

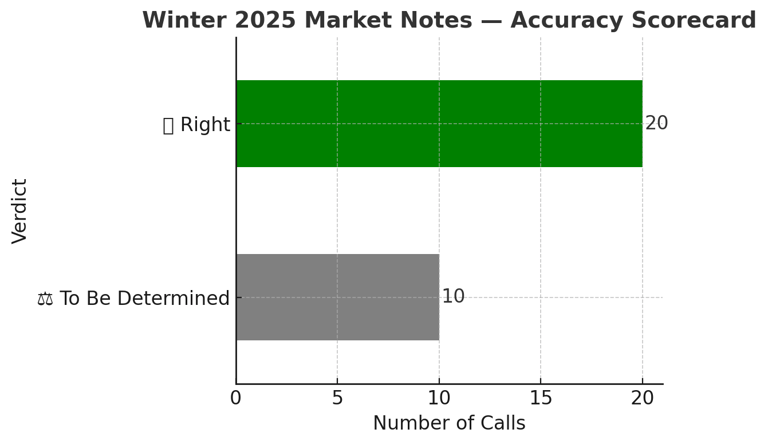

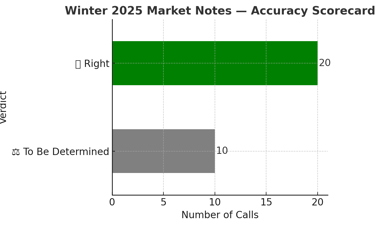

Nick's Market Notes:

Winter 2025 - Reviewed

Flight to quality continues — family homes outperform in freehold. ✅ Right — TRREB 416 detached market outperformed 905; A+ family homes still sell quickly.

Toronto to outperform suburbs as in-office continues to return. ✅ Right — 416 price declines smaller than 905; bank RTO mandates will reinforce this.

Over time people will choose higher living expense & city life over brutal commute. Commute times not improving. ⚖️ To Be Determined — Demand patterns support this, but still anecdotal.

Real estate sales to be incremental to begin year, no big bounce. ✅ Right — Q1 & Q2 growth was steady but unspectacular.

Toronto condo market to slowly improve from lower rates & RTO, lifting overall 2025 market. ⚖️ To Be Determined — Rates eased slightly, but condo performance still lags.

Equity stuck in condos negative for some freehold segments. ✅ Right — Investor capital remains locked in condo market.

Toronto truly bounces back when the condo market bounces back. ⚖️ To Be Determined — 416 stability holding without condo rebound, but sustained growth needs it.

Pre-sale condo market to remain weak. ✅ Right — Sales/launches still slow; absorption rates low.

Record new completions in 2025 will weigh on condo market. ✅ Right — Added inventory pressure in investor-heavy towers.

More shakeout in cities that ran up during pandemic. ✅ Right — Peripheral/exurban markets have underperformed.

Opportunity in Fixers. ✅ Right — Softer demand has created room for value creation.

Plenty of duplex/triplex options as ROI remain low & stocks rip. ⚖️ To Be Determined — Availability is there; returns vary widely.

Value in smaller, tweener freehold homes until condo rebound. ✅ Right — Still more liquid than condos in many areas.

Rec market will still be weak; choose quality. ✅ Right — Prime lakes outperform; fringe areas lag.

Opportunity to buy well-run condos w/newer infrastructure. ✅ Right — Boutique, well-managed buildings are holding value better.

Market fragmentation makes mistakes easier — or easier to know when to strike. ✅ Right — Highly segmented; micro-trends dictate success.

Sellers need patience. ✅ Right — Longer DOM unless property is prime.

First time in 2+ years market may slowly come to sellers. ⚖️ To Be Determined — Pockets are heating up, but not across the board.

Job market uncertainty for management/director class may impact $1.75M–$2.25M. ⚖️ To Be Determined — Too early to call clear impact.

Uninsured mortgage rule to $1.5M not immediately impactful. ✅ Right — No short-term effect.

Medium–long term stokes sub-$1.5M market unnecessarily. ⚖️ To Be Determined — Too soon to measure.

Pockets of strength to sell; timing matters. ✅ Right — Certain product types/locations outperforming.

Cost inflation & belt tightening still shape decisions. ✅ Right — Buyers remain price-sensitive.

US deregulation could spur growth & pull Toronto along. ⚖️ To Be Determined — Early days; no clear spillover yet.

Sellers remain under pressure to sell before buying. ✅ Right — Few bridge buys; financing still costly.

Cosmetic renos matter for home prep. ✅ Right — Well-prepped homes are moving faster.

Targeted marketing to right cohort critical. ✅ Right — Still essential in a segmented market.

‘Bumpy ride’/‘Vibesession’ labels unhelpful. ⚖️ To Be Determined — Sentiment remains cautious.

Federal election won’t affect RE decisions. ✅ Right — So far, no impact.

Trump tariffs to be negotiated but possibly recessionary; big unknown pre-inauguration. ⚖️ To Be Determined — Policy impact unclear.

Originally sent January 18, 2025. Verdicts based on August 2025 data and trends.